Research & Blogs

Should Your Family Office Leverage Gold to Combat the Eroding Purchasing Power of Cash?

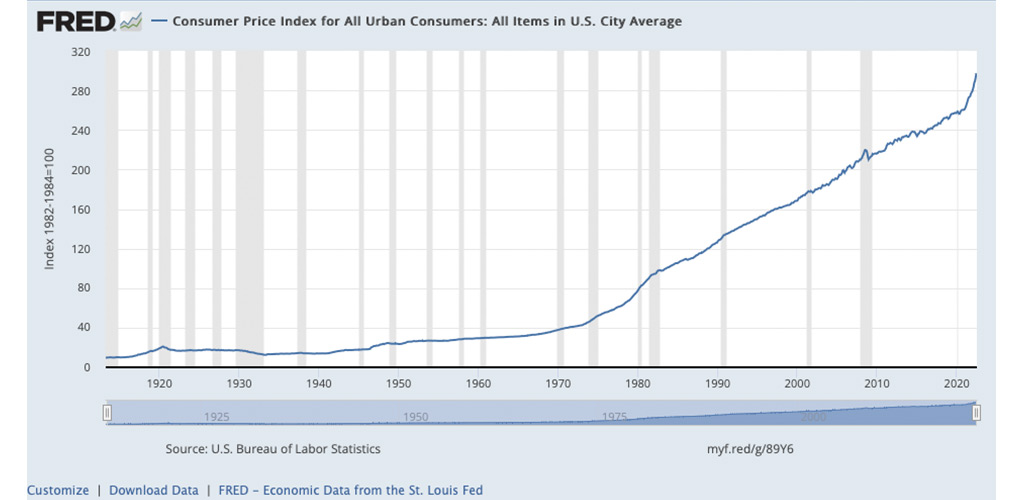

The Eroding Purchasing Power of Cash

Since the U.S. abandoned the gold standard in 1971, inflation has become a staple of our global economy. Even at low levels, it erodes the purchasing power of money. Family offices tend not to notice this constant threat, until rates of inflation spike. At times like these – 2022 – for example, family offices start asking pointed questions.

Hard Asset for Family Offices

Investments in property, like real estate, art, antiques or collectibles tend to perform well during periods of pronounced inflation. A Stanford University research review of Great Inflation of the 1970s and found inflation induced increase in housing investments. Art has shown similar strength. “The Art 100 Index“, by Art Market Research, shows art value shot up 130 percent from 1977 to 1982, while prices rose 80 percent.

What if you Need Greater Short-term Liquidity?

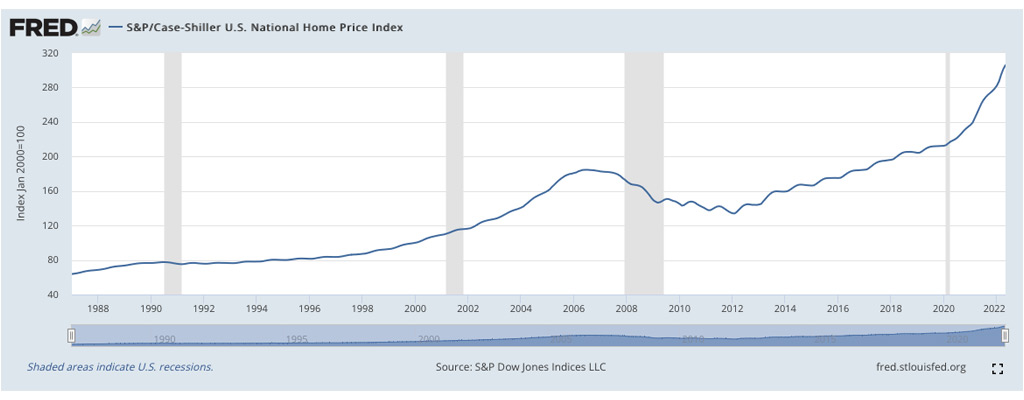

While the value of art, real estate, and other hard assets may increase during inflation, it is not easy or inexpensive to liquidate a property or a Picasso. And how comfortable can a family office be with real estate when the Case-Shiller Housing Index has been higher than December 2021 only once in over 140 years.

Plainly put, housing prices are hovering near all-time highs. Combine that with a jump in mortgage rates by as high as 400 percentage points and selling a home is easier said than done right now.

Is Investing Equities the Answer?

Over the long haul, stocks have indeed been a reliable safe harbor against inflation for family offices. But there have been long periods with inflation when stocks did not perform well. The “lost decade” following the domino effect of the dot-com bubble, terrorist attacks and Great Recession or the Great Depression are two great examples. With the juggernaut of macro economic factors dealt to the global economy, some fear we are at the precipice of a recession that will lead to another lost decade. Barry Bannister, the chief equity strategist at Stifel, believes that Covid, worldwide excessive spending, supply-chain disruptions, four-decade high inflation, geopolitical tensions, and regulatory pressure will eat any real returns for investors.

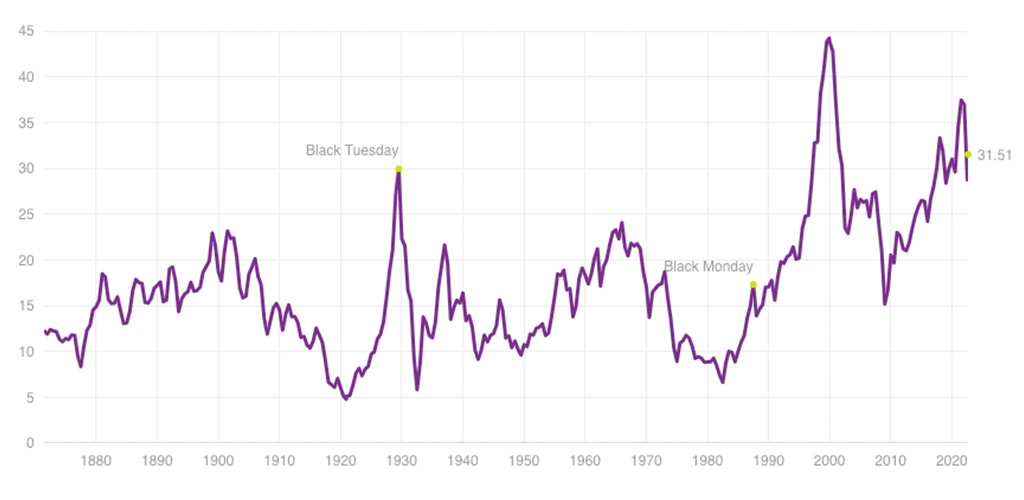

To further complicate the situation, we are at risk of stagflation combined with sky-high stock valuations. Calling upon Nobel laureate, Robert Schiller, once again, this time for his CAPE Ratio, we find that stocks have rarely been as highly valued as at the end of 2021. In fact, the only time since 1871 that stocks were as highly valued was prior to the Internet bubble at the turn of the millennium. Finally, inflation advice for a family office is usually more about reducing investment in cash that is being debased, than about taking on additional portfolio risk.

How comfortable is any family office in taking on more risk in a risk-off environment, especially in the face of pricey valuations?

What About TIPS

Treasury inflation protected bonds (TIPS) are built for the purpose of hedging against inflation, right? Well … yes and no. In June 2022, the Consumer Price Index hit 9.1% while 10-year US Treasury bond yields hovered under 2%. This means family offices hold bonds to maturity are signing up to lose over 7% in terms of purchasing power. This is a tough pill to swallow. TIPS are better, but still point to negative real yields. And what if central bankers around the world need to dramatically raise rates to combat unexpected inflation? Suddenly, the “risk-free” aspect of bond evaporates if a 40-year trend of declining rates is reversed.

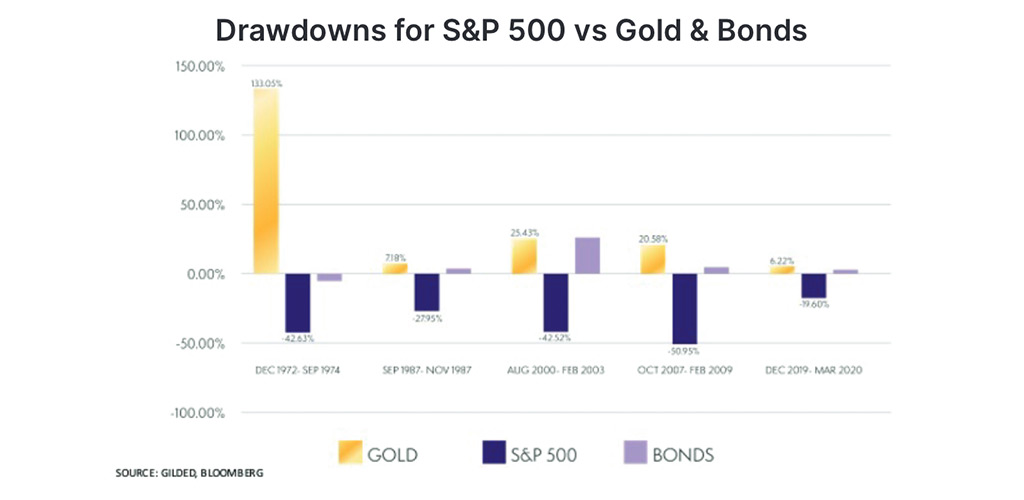

Maybe the Answer has Been Here all Along. Gold.

Gold offers a history of compelling returns even when compared against equities. Gold with a low historical correlation to market beta (stocks and bonds) offers a diversifying addition to most portfolios that could add to returns while lowering risk. This can be seen in the graphic below that examines a typical portfolio mix that benefits from higher expected returns and lower risk (yielding a higher Sharpe Ration) by reducing the portfolio allocation to cash by 5% and redirecting the investment to gold. And perhaps most germane to the conversation, Gold has historically done well during inflation and even better when inflation exceeded normal expectations. Like now.

Digital Gold

Digital gold is a new kid on the block that offers the best advantages of both physical gold and securities. This provides a unique investment strategy for you to preserve your family office wealth.

With digital gold, you own the gold outright as a physical asset.

However, where it differs is that you keep your gold in the company’s network, allowing you to pledge, collateralize, and monetize your gold position.

You have a yielding, bankruptcy-remote asset that maintains diversification and tail risk protection in extreme market stress by monetizing your gold, and arguably the most sound investment to preserve your family office wealth.

Start Investing Now

United States

1221 Brickell Avenue, Suite 900

Miami, Florida 33131

+1 (786) 233 5549

Channel Islands

IFC 5

St. Helier, Jersey JE1 1ST

Channel Islands

Abu Dhabi

Regus Al Maqam Tower

Al Maryah Island, Abu Dhabi Global Market Square

Al Maqam Tower, 3412Register13, 34th Floor

Abu Dhabi, United Arab Emirates![]() Whatsapp: +971.55.640.0950

Whatsapp: +971.55.640.0950

Copyright © 2022 Gilded. All Rights Reserved. Privacy Policy | Terms of Use